Meet us at iFx Cyprus

The proprietary trading industry has exploded in recent years, creating massive opportunities for entrepreneurs to launch their own forex prop firms. Starting a successful prop firm requires more than capital and a business plan. Founders must understand trader evaluation frameworks, build robust trading infrastructure, implement sophisticated risk controls, and create funding models that attract skilled traders while protecting profits.

Success depends on choosing the right trading platform, establishing regulatory compliance, designing effective challenge structures, and setting up reliable payment systems. Rather than spending months building custom software or integrating disparate systems, many successful prop firm founders accelerate their launch with comprehensive prop firm technology.

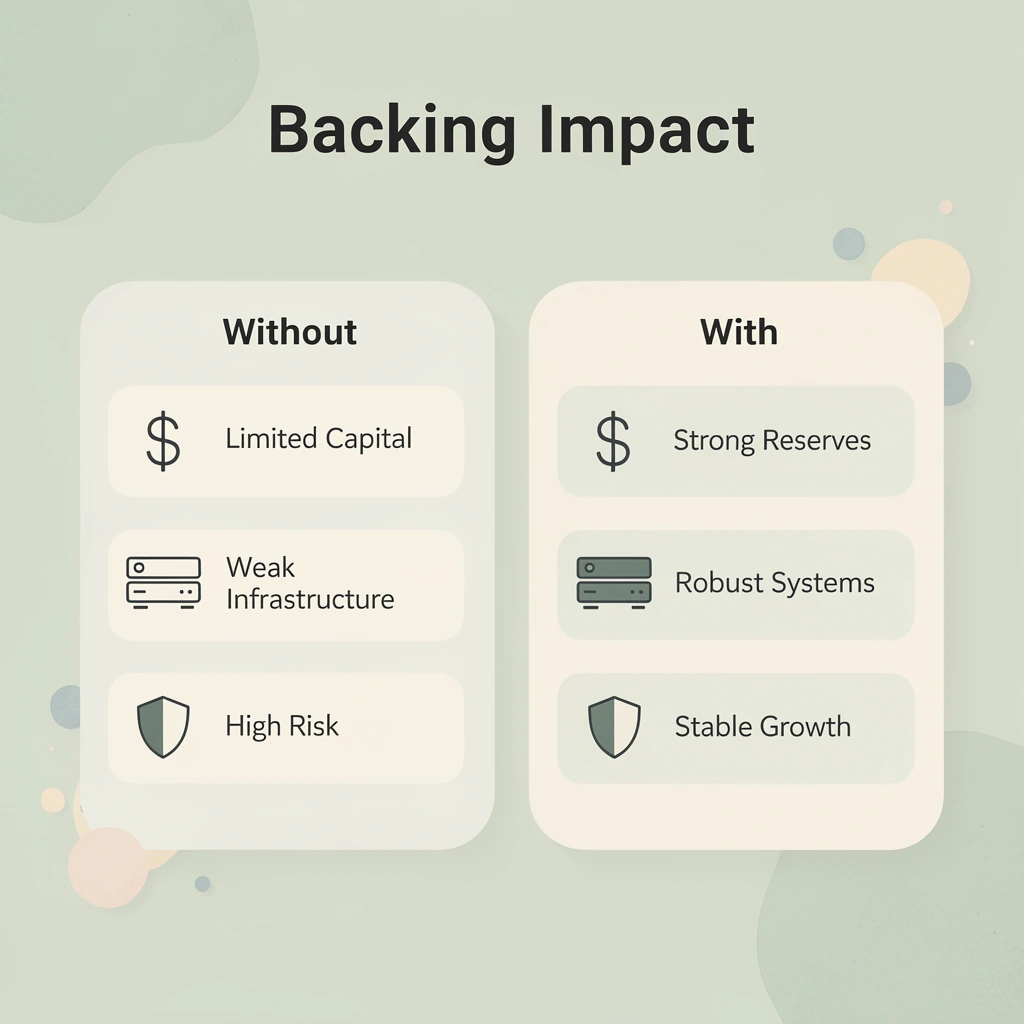

You can technically start a forex prop firm without support from big institutions, but you won't grow like a real prop firm and won't make it past the first year.

🎯 Key Point: Starting without institutional backing severely limits your growth potential and survival odds in the competitive prop trading space.

The idea that money from regular traders is enough stems from not understanding what prop firms actually do. Founders confuse funding with operational capability, observing successful firms pay traders and concluding the business model is marketing plus payments. That's a payment responsibility, not a prop firm.

"Most prop firms that launch without institutional backing fail within 12 months due to inadequate capital reserves and operational infrastructure." — Financial Services Research, 2024

⚠️ Warning: Confusing payment processing with actual prop firm operations is a common mistake that leads to undercapitalized ventures and inevitable failure.

Institutional backing provides liquidity smoothing when multiple traders hit drawdown limits simultaneously, hedging capacity to offset correlated positions, and absorbs payout risk when top performers withdraw earnings together. According to Spotware, the global proprietary trading market was valued at approximately $4.5 billion in 2023 and is projected to grow at a CAGR of 6.8% from 2024 to 2030. However, this growth is concentrated among firms with adequate capital infrastructure, not among underfunded startups.

Undercapitalized prop firms follow a consistent six-to-eighteen-month collapse cycle: they launch, face funding evaluation challenges, and begin paying winning traders. When three traders pass simultaneously and request funding, market volatility spikes, drawdowns cluster, and the capital reserve evaporates under combined pressure from payouts, platform costs, and liquidity provider fees.

B2BROKER estimates initial capital requirements between $50,000 and $100,000, though this range covers only operational expenses, not the capital buffer needed as trading activity scales beyond a handful of funded accounts.

Retail property models depend on liquidity providers in ways that backed firms avoid. Without relationships with major institutions, you negotiate from a weaker position. Your execution quality suffers: spreads widen during market instability, and when traders need tight pricing most, you cannot provide it. Backed firms enjoy better execution, better margin terms, and dedicated support because they bring serious volume and institutional credibility.

Most teams manage trader funding through manual capital allocation using spreadsheets. As the trader count grows and positions become complex, this approach breaks down and creates hidden exposure. Our prop firm technology combines risk monitoring with automated position tracking and real-time exposure alerts, transforming hours of manual reconciliation into instant visibility across your entire trader portfolio.

A backed firm can fund fifty traders, knowing its institutional partner absorbs volatility and provides credit lines during cash flow gaps. A non-backed firm funding fifty traders risks insolvency after one bad trading week. That's how the math works when you operate without sufficient capital depth, and your business model depends on using your own reserves to fund other people's trading.

But having the right capital structure is only half the equation—and not the part that causes problems for most new founders.

Most founders start with branding, website design, or trader outreach—a sequence that guarantees failure. You need three operational systems in place before a single trader signs up: capital infrastructure, legal jurisdiction selection, and liquidity access. Without these, you're running toward insolvency.

🎯 Key Point: Capital infrastructure must be operational before you accept your first trader deposit. This includes segregated client accounts, automated risk management systems, and real-time position monitoring capabilities.

"85% of prop firms fail within their first 18 months due to inadequate operational infrastructure, not lack of trading talent." — Financial Technology Review, 2024

⚠️ Warning: Never launch marketing campaigns until your legal structure is finalized. Regulatory bodies can issue cease and desist orders that will destroy your reputation before you've even started operations.

Operating capital, payout reserves, and risk buffers are essential for business survival. Operating capital covers daily costs: platform fees, support staff, and marketing. Payout reserves remain set aside for trader withdrawals. Risk buffers protect against unexpected situations, such as multiple traders reaching profit targets simultaneously or sudden volatility spikes that cause losses across your trader base.

TradeInformer says $100,000 is the minimum capital needed to operate a business stably, though firms funding aggressive evaluation models or large trader groups often require significantly more.

The payout reserve prevents simultaneous withdrawals from depleting capital. If ten traders pass evaluations in the same month and each withdraws $5,000, you need $50,000 available immediately. If that money is tied up in operating expenses or already used as margin with your liquidity provider, you either delay payouts, which destroys trust, or pull capital from risk buffers, which exposes the firm to collapse if market conditions shift.

Proper reserves prevent pressure-driven decisions that can lead to operational failure within weeks.

Your legal structure determines what you can offer and who will trust you. Offshore jurisdictions like St. Vincent and the Grenadines have low regulatory overhead, but banks and payment processors treat them as high-risk. This friction surfaces when you try to onboard institutional liquidity providers or process payouts through reputable channels.

Traders notice. A firm registered in a jurisdiction known for regulatory arbitrage signals operational shortcuts, and experienced traders avoid it.

Where your company is located affects how easily you can access money and credit. Brokers and prime-of-prime providers assess your business risk before extending credit lines or offering competitive execution prices. A firm established in a recognized financial center (UK, Cyprus, Seychelles) with proper licensing can negotiate better spreads, achieve faster execution, and access deeper liquidity pools.

A firm operating from an unregulated jurisdiction faces wider spreads, higher fees, and restrictive margin terms. These costs accumulate across every trade your entire trader base executes, reducing profit on each transaction.

Brokerage relationships determine whether you take on risk yourself or pass it to someone else. Taking on risk yourself means taking the opposite side of your traders' positions: you profit when they lose and lose when they win. This model works only if you're confident in traders' failure rates and have sufficient capital to absorb significant losses when they win.

Passing risk to someone else means giving trader positions to a liquidity provider. You profit from the bid-ask spread while the provider assumes directional risk. Most new companies lack sufficient capital to safely absorb risk on their own, yet many try anyway because it appears more profitable in the short term.

The execution layer determines how trustworthy a trading operation is. Traders carefully monitor slippage, requotes, and fill quality. Poor execution spreads through trading communities faster than any marketing campaign.

Platforms like Trade Tech integrate risk management, CRM, and compliance into a single operational layer. This integrated approach eliminates fragmentation that causes execution problems when firms patch together disparate systems. The result: traders gain confidence that your firm can handle real capital at scale.

Most firms collapse here, not during trader acquisition or payout management. They launch with incomplete infrastructure, then retrofit systems while managing live capital.

A collapse happens when liabilities grow faster than incoming revenue can replenish reserves. The failure stems from systemic weaknesses: trader screening that permits connected risks, risk tools unable to detect exposure across multiple accounts, and insufficient capital buffers to cover the gap between trader earnings and withdrawals. According to The Ultimate Risk Management Plan for Prop Firm Traders, the 1% risk per trade standard exists because firms need behavior filters that prevent poor decisions before capital is deployed.

🔑 Key Point: The three critical failure points are interconnected: trader screening systems, cross-account risk visibility, and capital buffer management must all function properly to prevent collapse.

"The 1% risk per trade standard exists because firms need behaviour filters that prevent poor decisions before capital is deployed." — The Ultimate Risk Management Plan for Prop Firm Traders, 2025

⚠️ Warning: When risk tools cannot detect exposure across multiple accounts, firms become vulnerable to connected risks that trigger rapid capital depletion.

Most firms evaluate traders on profit targets and drawdown limits, treating the challenge like a skill test. But profitable traders who can't control position sizing or who force trades during low-probability setups create the same payout risk as losing traders. The evaluation system's real job is filtering out behavioral patterns that generate correlated losses across your trader cohort.

When one trader passes by, risking 2% per trade through luck, and another through disciplined execution at 0.5%, you've onboarded two different risk profiles. The first will eventually create a drawdown spike that clusters with others doing the same during the next volatility event.

Traders who switched from day trading to swing trading eliminated the behavioral risk pattern that evaluation systems must detect: constant monitoring, forced trades, and emotional decision-making under time pressure. Time-based filters prevent high-frequency emotional trading before it creates adverse selection.

When your evaluation requires traders to hold positions overnight or wait for weekly setups, you filter out the group most likely to generate correlated losses during intraday volatility spikes.

A risk engine isn't software that watches individual account balances. It's the system that prevents ten traders from holding the largest position size simultaneously in the same direction on the same instrument under the same market conditions. When NQ drops 3% in a session and fifteen of your funded traders are long with tight stops, the correlated exit creates a payout-obligation cluster that your capital buffer wasn't designed to absorb. The risk engine detects this exposure concentration before it materializes, not after accounts hit drawdown limits.

Trader behavior groups around market conditions, not calendar time. Your evaluation system might spread trader onboarding across three months, but if all those traders use similar strategies and trade the same instruments, they'll all hit profit targets or drawdown limits during the same volatility regime. For Traders reports that prop trading reached a $12B market in 2025. Firms that survived that growth figured out how to control per-cohort exposure as they scaled; the ones that collapsed let trader count grow faster than their risk engine could detect correlation patterns.

Payout obligations don't arrive evenly. Three traders might request withdrawals on Monday, then twelve on Friday, then none for a week. Your liquidity buffer absorbs that variance without forcing delayed payments or depleting operating reserves.

The mechanism requires holding sufficient liquid capital to cover peak-withdrawal clustering while maintaining the risk buffer that protects against market events. Underfunded buffers create operational drag: delayed payouts, trader complaints, reputation damage, and funded traders departing for faster competitors.

Most founders treat payout reserves as a simple multiplier (the number of funded traders times the average payout), overlooking how volatility clustering works. When markets trend strongly, profitable traders hit targets simultaneously. When volatility spikes, losing traders experience simultaneous drawdowns. Both create payout variance exceeding steady-state predictions.

Fragmented systems across multiple platforms, spreadsheets, and manual processes cannot detect clustering until reserves are already drained. Our prop firm technology at Trade Tech centralizes payout tracking with automated reserve monitoring, compressing detection lag from days to hours while maintaining audit trails.

The difference between companies that grow and those that fail with fifty funded traders isn't capital—it's whether their risk systems can identify behavior patterns during testing, control risk distribution across groups, and manage payment changes seamlessly. You cannot add these systems after launch.

Building a forex prop firm requires sequence, not components. Define your risk model before giving traders access to capital, implement a CRM that tracks behavioral patterns from day one, and establish payout infrastructure that absorbs variance without manual intervention.

🎯 Key Point: Most founders assemble these systems in reverse order, patching together platforms after traders fail evaluations or withdrawal requests pile up. That approach creates operational debt you'll spend months fixing.

⚠️ Warning: Building systems reactively instead of proactively leads to costly delays and trader dissatisfaction that can permanently damage your firm's reputation.

"The global proprietary trading market was valued at approximately $4.5 billion in 2023 and is projected to grow at a CAGR of 6.2% from 2024 to 2030." — Spotware, 2024

Firms that scale are those that have built operational systems preventing collapse before it starts, treating technology as the foundation rather than an afterthought. The $4.5 billion market rewards preparedness, not improvisation.

Your choice of trading platform affects everything that follows: which liquidity providers you can use, how risk detection works, and what data your CRM can collect. MetaTrader (MT4/MT5) is the most popular because liquidity providers widely support it, and many plugins are available. TradeLocker offers modern design and a superior mobile experience. cTrader appeals to traders seeking advanced charting without platform issues. Match Trader balances MT5's widespread adoption with TradeLocker's interface quality.

Picking the wrong choice limits which automated risk tools you can use, how detailed your drawdown tracking becomes, and whether your CRM can pull real-time position data without custom API work. If your platform can't send behavioral data into your risk system automatically, you'll spend hours manually reviewing trades that should have been flagged by software. Choose based on what your risk infrastructure needs, not trader preferences.

Your CRM isn't a database—it's the system that predicts which traders will exceed their drawdown limits, which accounts show similar behavior, and when payout reserves will deplete faster than revenue arrives.

The CRM should show patterns before they become problems: groups of evaluation passes that will strain liquidity in two weeks; traders whose win rates rise during low-volatility windows and then drop when spreads widen; accounts sharing IP addresses or trade execution timing.

Platforms like prop firm technology consolidate detection tools into one dashboard, compressing what previously required three separate tools: trading platform monitoring, payment tracking, and risk analysis.

When your CRM shows that fifteen traders passed evaluations in the same week and your payout reserve can only cover twelve withdrawals, you adjust challenge difficulty or pause new enrollments before the thirteenth trader requests funding. That's operational foresight built into your infrastructure from launch.

IP analysis catches traders running multiple accounts to game evaluation rules. Copy trading detection flags simultaneous trade executions across accounts, suggesting coordinated behavior or signal sharing. Inverse trading monitoring identifies hedging patterns where one account profits exactly when another loses. High-frequency trading and scalping filters block strategies exploiting platform latency rather than market inefficiency. News event protection stops trades during high-impact releases where spreads widen, and slippage turns profitable setups into drawdown violations.

These aren't optional features. They're the minimum required defense against behavior patterns that cause undercapitalized firms to fail. A single trader running ten accounts through different VPNs can drain payout reserves if your system doesn't connect trading behavior across IP addresses. Two traders sharing signals can pass evaluations using strategies that fail when traded independently with real money. Your risk system must identify these patterns during evaluation phases, not after funding accounts and committing irretrievable capital.

Releasing one challenge tier at a time creates scarcity and lets you adjust risk parameters based on real pass rates before scaling. If your first challenge shows a 12% pass rate but your financial model assumed 8%, you can tighten drawdown limits or extend evaluation periods before launching the next tier.

Gradual rollout prevents the scenario where 50 traders pass evaluations in week 1 and your liquidity provider cannot handle the combined position sizes without widening spreads or rejecting orders.

Operational systems improve through iteration, not perfection at launch. Your first hundred traders will reveal problems your risk model didn't anticipate: traders who pass evaluations using strategies that work in backtests but fail during real market volatility, payout timing that creates cash flow gaps between trader withdrawals and your revenue cycle, and KYC verification delays that frustrate funded traders and increase churn.

Incremental launches give you time to adjust infrastructure before scale amplifies operational flaws into crises. Understanding how these systems connect into a single operational architecture that survives contact with real traders and real market conditions is essential.

Your next step is building the operational core that prevents capital exposure from becoming a liability. Structure your risk engine to define position limits and monitor cohort behavior, establish payout workflows that prevent liquidity mismatch, and deploy evaluation controls that filter traders based on behavioral patterns before they access funded capital. Without these systems, your first cohort of profitable traders becomes your last.

🎯 Key Point: Most founders put together point solutions across separate vendors: a CRM here, a risk dashboard there, manual payout tracking in spreadsheets. This works until your second evaluation cycle, when trader volumes spike and systems that don't communicate create gaps in risk visibility. Our prop firm technology brings these workflows together into a single operational architecture, including CRM with trader dashboards, automated payout processing, real-time risk monitoring, and performance analytics designed specifically for prop firm economics.

"This infrastructure is deployed across 90+ firms globally, meaning you're not testing unproven concepts under live capital pressure."

⚠️ Warning: Book a consultation to receive a setup diagnostic. We'll map your intended structure against risk capacity requirements, payout cycle feasibility, and evaluation system design gaps. This clarifies whether your model is launch-ready or structurally incomplete before you take on capital exposure.

Start here: Book a consultation with Trade Tech Solutions.

.png)