Meet us at iFx Cyprus

The proprietary trading industry has exploded in recent years, creating unprecedented opportunities for entrepreneurs who understand both markets and business operations. Thousands of traders and business-minded individuals are recognizing the potential to build sustainable, scalable ventures that fund talented traders while generating consistent returns. Opening a prop firm requires establishing legal foundations, crafting risk-management frameworks that protect capital, designing profit-sharing models that attract top-tier talent, and implementing operational systems that distinguish hobbyist ventures from institutional-grade businesses.

Building the infrastructure for a successful prop firm used to require massive upfront investment and months of technical development. Modern solutions now provide ready-to-deploy platforms that handle trader evaluation, risk monitoring, payout processing, and compliance tracking. These tools let founders focus on strategy, trader recruitment, and business growth rather than wrestling with backend systems. Trade Tech Solutions offers comprehensive prop firm technology built specifically for founders who want to launch quickly without sacrificing the professional standards that serious traders expect and regulators demand.

Yes, you can open a prop firm, but not the way most people think. Most assume it's as simple as buying a trading platform, setting up a website, and giving money to traders. In reality, the business runs on challenge fees and monthly subscriptions that generate steady revenue independent of market performance. According to research from Leverate, 90% of prop firms fail within the first year, not from lack of technology, but from payout obligations they never anticipated.

"90% of prop firms fail within the first year, not because they couldn't afford technology, but because they collapsed under payout obligations they never planned for." — Leverate Research, 2024

🔑 Key Takeaway: The prop firm business model is fundamentally a subscription and fee-based operation, not a traditional trading business. Success depends on managing cash flow and payout ratios, making financial planning and risk management the most critical factors for survival.

⚠️ Warning: Many aspiring prop firm owners underestimate the capital requirements needed to handle trader payouts during profitable months. Without proper reserve funds, even successful trader performance can bankrupt your firm.

The math reveals the actual business model. A company with 10,000 funded traders, charging $150 per month in subscription fees, generates $1,500,000 in recurring revenue before any trades occur. For each funded account, approximately 100 traders fail the $100 challenge, generating $100,000,000 in one-time revenue. According to research from Spotware, the global proprietary trading market was worth $4.5 billion in 2023 and is expected to grow at a CAGR of 6.2% from 2024 to 2030, driven primarily by this evaluation-based revenue model. Profit-split arrangements with successful traders (10-50% of gains) represent supplementary income, not the primary source.

Prop firms create three types of traders that determine profitability. The "best" traders lose money and repeatedly face new challenges, generating pure revenue with no payouts. The "acceptable" traders achieve 1-2% monthly returns, low enough that challenge fees cover withdrawals while demonstrating that "real traders succeed here." The "worst case" traders pursue 8-10% returns, creating an unfavorable money-to-results ratio where a $400 challenge fee must cover an $8,000 payout on a large account.

Strict trading rules protect this financial model by ensuring most traders either lose their accounts or generate profits small enough to keep payouts manageable. Consistently high returns become a problem that threatens the firm's sustainability. The business relies on statistical predictability: if 80% of new traders fail within the first year, firms can reliably forecast income against obligations.

The challenge model works well because it converts goals into immediate revenue. Traders pay upfront for evaluation, which funds operating costs (technology infrastructure, payment processing, compliance tracking, risk management) across multiple failed attempts before successful traders receive funding. Subscription fees from funded accounts then generate steady, scalable income as the trader base grows.

Platforms like prop firm technology handle this financial infrastructure through integrated systems that track challenge participation, automate payout calculations based on profit-split arrangements, and maintain compliance across thousands of simultaneous evaluations. Without this technical backbone, firms cannot manually process challenge fees, monitor loss limits, calculate profit distributions, and maintain audit trails at scale.

The idea that you need substantial capital to start a prop firm stems from conflating trader money with operational costs. Many firms launch with modest initial investment directed toward technology platforms, trader evaluation systems, and training infrastructure.

The challenge model pays for itself: early participants pay for the software that tests later participants, covering the business's operating costs before real money is deployed for trading.

This explains why data from B2BROKER shows startup costs ranging from $5,000 to $50,000, with the main focus on licensing the appropriate technology stack. The business model works because you collect fees from many traders to fund payouts to the few who succeed, rather than risking capital on every trader.

But getting the financial structure right is only half the equation; the technical systems that enforce these rules determine whether your firm survives its first year.

Making money depends on three connected parts: your pass rate for evaluations, how you organize payout liability, and your acquisition cost per trader. If 1,000 traders pay $200 for evaluations and 10% pass, you've generated $200,000 in revenue. Those 100 funded traders represent potential payout obligations that must remain below that amount for the model to work. When one trader withdraws $8,000 under an 80/20 split, the unit economics fail unless dozens of failed attempts funded that single payout.

🎯 Key Point: The profitability equation is simple: evaluation fees from all traders must exceed total payouts to successful traders, plus operational costs.

"If 1,000 traders pay $200 for evaluations and 10% pass, you've made $200,000 in revenue - but those 100 funded traders represent potential payout obligations that must stay below that threshold."

🔑 Takeaway: Low pass rates are essential for prop firm survival - when 90% of traders fail their evaluations, their fees subsidize the payouts to the successful 10%.

According to Best Prop Firms, the prop trading industry is worth approximately $20 billion globally, with over 2,000 firms operating across different countries. Most revenue comes from evaluation fees paid by traders who never achieve funded status.

The 5-15% pass rate allows failed challenge fees to create a capital pool large enough to cover successful traders' withdrawals. A $50,000 evaluation priced at $300 reflects the statistical likelihood that nine others will fail for every one who passes, with their fees funding that winner's capital allocation.

Pass rates above 20% invert the model: you're funding more traders than evaluation revenue can support, creating a liquidity crisis unless acquisition volume scales faster than the growth of funded traders.

An 80/20 profit split sounds appealing for traders until you examine what happens when funded traders generate substantial returns. A trader who consistently makes 8-10% monthly on a $100,000 account creates $8,000–$10,000 in profit, meaning the firm owes $1,600–$2,000 per month under that split.

If your cost to acquire each trader was $400 (the average challenge fee after accounting for pass rates), you're paying four to five times what you collected to fund that account. The model works only when most funded traders either fail within their first few months or generate returns so small that the 20% firm share remains below the amortized cost of acquiring that trader.

Research from Best Prop Firms shows that 62% of prop firms are based in the United States, where regulatory scrutiny around payout structures is intensifying. Firms cannot deny payouts when traders succeed.

The structured imbalance depends on the 60-80% failure rate of the account. When traders breach drawdown rules or violate risk parameters, they exit the system, and the firm retains the evaluation fee without ongoing payout liability.

Traders who stay within risk limits and generate 1-2% monthly returns become sustainable. Those who swing for 8-10% become liabilities, not because they're winning, but because their payout magnitude exceeds what the evaluation funnel economics can cover.

Every funded trader represents a bet that their lifetime payout stays below the revenue their cohort generated through failed evaluations. If you spend $500 in marketing and platform costs to acquire a trader who pays $200 for a challenge, your true acquisition cost is $700. When that trader passes and requests a $5,000 withdrawal after three months, you're $4,300 underwater on that individual.

The math only works if 20+ other traders in that cohort failed their evaluations, contributing $4,000+ in fees that never converted into payout obligations. This is why firms focus on pass rates and why prop firm technology that tracks cohort-level profitability across evaluation funnels, payout cycles, and trader lifecycles becomes operationally critical. You're managing statistical pools where aggregate intake must exceed aggregate outflow.

Traders who repurchase evaluations after failing to do so become the most profitable customer group. A trader who buys three $200 challenges before passing contributes $600 to the capital pool. Even if they eventually withdraw $3,000, the firm breaks even faster than if they had passed on the first attempt.

This explains why some firms offer cheaper retries: each failed attempt strengthens the capital pool that funds successful traders. Understanding how money flows through evaluation funnels and payout structures reveals only half the operational picture. The systems that enforce these economics determine whether your firm survives its first year.

Without the right infrastructure, you're not running a prop firm—you're running a countdown to insolvency. Four systems determine whether you survive your first payout cycle or join the 90% that collapse within twelve months.

⚠️ Warning: The infrastructure gap is where most prop firms fail. Risk management systems, trader monitoring platforms, payment processing, and compliance frameworks must work in perfect harmony—or your firm becomes another failure statistic.

"90% of prop firms collapse within twelve months due to inadequate infrastructure and risk management failures." — QuantVPS Industry Report, 2024

🔑 Takeaway: Your core systems aren't just operational tools—they're the foundation that determines whether you're building a sustainable business or a house of cards waiting for the first major drawdown to destroy everything.

A risk engine controls how much capital sits exposed at any moment across all traders. Without it, correlated wins create payout clustering that destroys liquidity stability. When ten traders using the same breakout strategy all profit on the same XAUUSD move, they trigger simultaneous withdrawal requests that your cash reserves cannot honor. Your risk engine must limit aggregate exposure per instrument, per session, and per strategy type. If five traders are long gold during the London open, the sixth faces position-size restrictions or outright blocks until correlation risk drops.

An evaluation system controls who gets funded and who stays in the challenge pool. Without it, you fund traders whose edge disappears after 100 trades. A coin-flip strategy with zero edge passes the prop firm's challenges 45% of the time, with a small sample size. This mirrors subprime mortgage lending, where banks lacked underwriting standards and funded borrowers destined to default. Your evaluation system must distinguish between a trader who passed one challenge through luck and one who demonstrates repeatable edge across multiple instruments and volatility regimes.

A liquidity buffer controls the gap between trader withdrawals and incoming evaluation fees. Successful payout requests during low-revenue periods can trigger liquidity crises, similar to bank runs, in which withdrawal demand exceeds available reserves. According to propfirmapp.com, prop firms have paid out $2.5 billion total, but individual firms face distinct timing risks. If your best traders request payouts when new challenge sales drop, you need reserves absorbing 30–60 days of negative cash flow. Our prop firm technology integrates payment processors with payout-scheduling tools, enabling firms to model liquidity-stress scenarios before cash shortfalls occur.

A trader lifecycle funnel controls how participants move from evaluation to funded to scaled accounts. Without clear advancement paths, traders stagnate and churn. Your funnel must define what triggers each transition: passing one challenge versus three, maintaining specific win rates, or hitting profit targets without violating drawdown limits.

Traders who pass their first evaluation but fail to grow within 90 days need different help than those who lose their accounts in week one. The lifecycle funnel separates these groups so you're not treating a discipline problem the same as a strategy problem.

These four systems create the operational capacity that separates firms operating at over 2,000 worldwide from those that never progress past their first hundred traders.

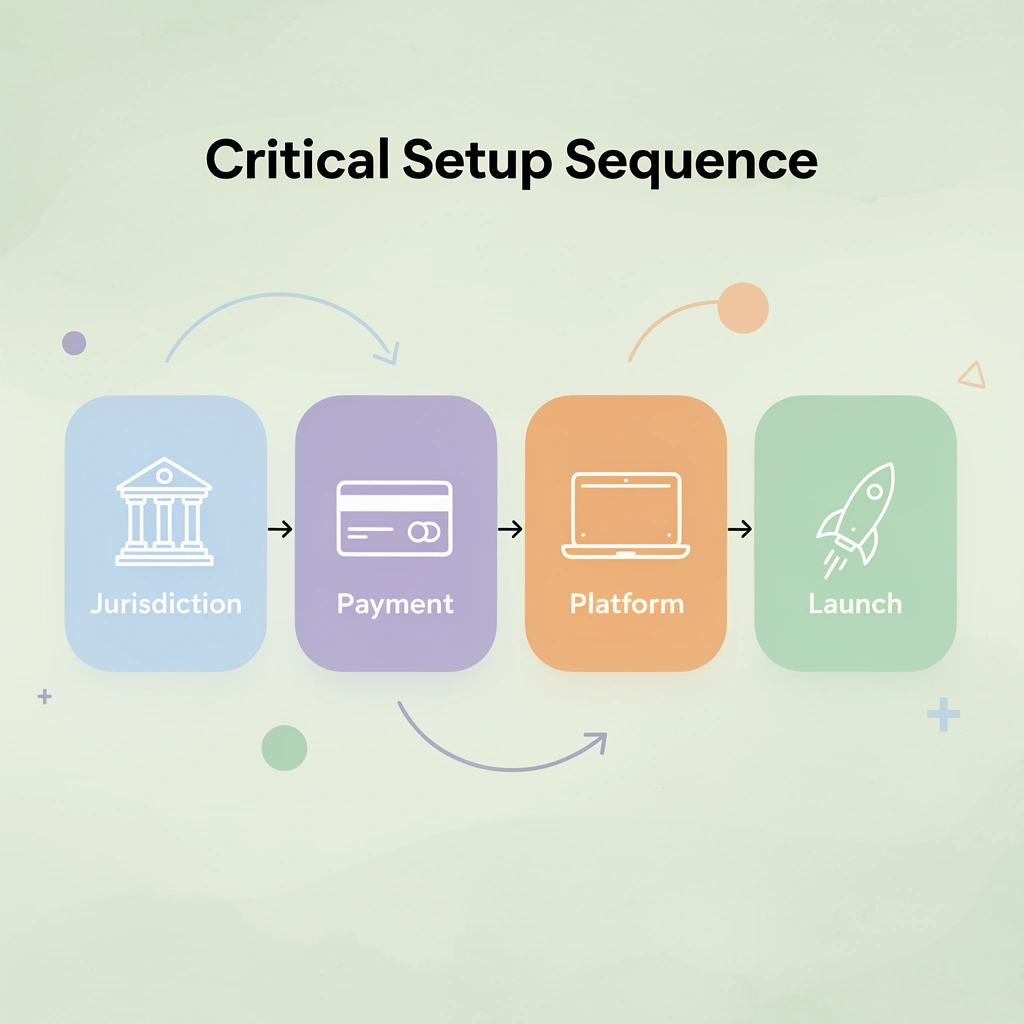

The order of steps matters more than the tools you pick. Choosing a platform before picking your jurisdiction blocks payment processors. Making evaluation rules without understanding how liquidity buffers work creates problems that worsen. Jurisdiction affects payment stability, payment stability affects payout reliability, and payout reliability determines whether you survive your first hundred funded traders. Skip a step or do them in the wrong order, and you're building on a foundation that can't support what comes next.

🎯 Key Point: The sequence of your setup decisions creates a domino effect - each choice either strengthens or weakens your operational foundation.

"Jurisdiction affects payment stability, payment stability affects payout reliability, and payout reliability determines whether you survive your first hundred funded traders."

⚠️ Warning: Reversing setup decisions later costs 10x more in time and resources than getting the initial sequence right from the start.

Start with where you'll incorporate and what type of entity you'll use, as these decisions control your regulatory exposure and payment processing options. A Delaware LLC offers different banking relationships than a Saint Vincent entity. Some jurisdictions unlock Stripe and PayPal integration, while others force you into crypto-only payment rails or high-risk merchant accounts with 7% fees and rolling reserves.

According to research from the International Compliance Association (2024), payment processor rejection rates for financial services entities vary by 300% depending on the jurisdiction of incorporation.

Match your target market to payment infrastructure that can serve them. If 80% of your customers will pay with U.S. credit cards, incorporating in an offshore jurisdiction that blocks U.S. payment processors creates a structural problem no marketing budget can solve.

Fintech legal specialists can map the relationship between your choice of incorporation and the payment methods you'll need, preventing costly disqualification by the processors your customers expect.

Your risk model determines survival under variance: calculating how many failed evaluation fees fund each successful trader's withdrawals, what maximum drawdown limits prevent correlated blowups, and how profit targets filter skill from luck. If your model assumes a 10% pass rate but real behavior produces 18%, your liquidity drains faster than revenue replenishes it. A trader who passes a $100 evaluation and withdraws $8,000 over six months requires 80 failed attempts at that same evaluation level to break even, assuming zero operating costs.

Design this before setting evaluation prices or withdrawal rules. The payout model defines the profit curve and answers whether you can afford to pay traders who pass, or whether you depend on high failure rates to stay solvent. Many firms launch with rules that feel "competitive" without stress-testing them against realistic pass rates and withdrawal patterns. When traders start succeeding, the model collapses. Actuarial thinking matters: you're building an insurance pool where premiums (evaluation fees) must cover claims (payouts) plus operating costs, with sufficient margin to survive variance when multiple funded traders have winning months simultaneously.

Evaluation rules determine how your traders distribute capital and profits. A $10,000 challenge with a 10% drawdown limit and a 30-day constraint yields a different pass rate than the same account size with a 5% drawdown and no time limit. Tighter rules reduce pass rates but may lower conversions if traders perceive them as unfair. Looser rules increase pass rates but compress your margin between evaluation revenue and payout obligations.

According to proprietary data from multiple prop firms analyzed in 2024, every 1% increase in evaluation pass rates requires approximately 15% more failed attempts to maintain the same profit margin.

Don't copy competitor rules without understanding how they work with your Step 2 model. If your risk model assumes an 8% pass rate but your evaluation rules historically produce a 14% pass rate in live environments, you've created a mismatch that manifests as liquidity stress three months after launch.

Test rules against historical trading data. Simulate how different profit targets and drawdown limits affect the distribution of outcomes. The goal is to align difficulty with the payout obligations your revenue model can sustain. Challenge design is actuarial engineering, not marketing.

A liquidity buffer prevents payout shock failure: the capital reserve that covers withdrawal requests when multiple funded traders have profitable months before new evaluation revenue arrives. Firms fail here more than anywhere else, not because they lack revenue, but because the timing of revenue doesn't match the timing of payouts. A trader who passes in January and requests withdrawal in February gets paid from your reserves, not from February's new evaluation sales. Without reserves, you're forced into delaying payouts, selectively enforcing rules, or hoping enough traders fail to cover the ones who succeed.

Size this buffer based on maximum simultaneous payout exposure. If you have 100 funded traders with $2,000 average monthly payouts, you need liquid capital to cover 20 simultaneous withdrawal requests in one week—$40,000 in cash flow demand that cannot wait for next month's evaluation revenue. Many operators underestimate this by focusing on total profitability rather than cash flow timing. You can be profitable on paper and insolvent in practice if payout obligations arrive before revenue does. The buffer is the difference between paying traders on time and becoming another case study in why prop firms collapse.

Launch means going live with real traders and real money to test whether your theoretical model matches actual behavior. Calibration is the process of adjusting evaluation rules, payout terms, or risk limits based on real-world interactions with your system.

The gap between projected and actual pass rates reveals whether your Step 3 design works. The gap between projected and actual withdrawal timing reveals whether your Step 4 buffer is adequate. Most firms discover these gaps only after launch, since traders' behavior cannot be perfectly predicted in advance. You build a model, test it against reality, and adjust.

Tools that track pass rates by account size, average time to failure, withdrawal request timing, and profitability by trader group provide the data needed for calibration. If 30-day challenge pass rates reach 22% when modeled for 12%, tighten the rules, increase evaluation prices, or expand your liquidity buffer.

Tightening rules may reduce conversions. Increasing prices may reduce volume. Expanding buffers requires more capital. Calibration isn't about avoiding tradeoffs—it's about making them intentionally, based on real data, rather than discovering them as crises when payout obligations exceed your cash position.

But knowing the sequence matters only if you understand the infrastructure decisions that make each step executable.

The operational structure you map today determines whether your prop firm launches cleanly or collapses under its first wave of payouts. You need systems connecting evaluation logic to risk controls, payout workflows to trader analytics, and retention tracking to liquidity forecasting. This infrastructure executes the sequence you've already designed: from trader onboarding through funded account management to withdrawal processing.

🎯 Key Point: Your infrastructure must seamlessly connect every operational component—from trader evaluation to risk management to payout processing—without requiring manual intervention at scale.

Prop firm technology built for this stage includes CRM dashboards that track trader progression, risk management systems that monitor correlated exposure, payout workflows that automate withdrawal approvals based on predefined thresholds, and platform integrations that connect MT4, MT5, cTrader, and DXtrade accounts to your evaluation rules. Our infrastructure helps firms scale: the difference between firms that scale and firms that stall often comes down to whether their systems can handle 500 active traders without manual intervention in payout decisions or risk adjustments.

"The difference between firms that scale and firms that stall often comes down to whether their systems can handle 500 active traders without manual intervention." — TradeTech Solutions, 2024

⚠️ Warning: Manual intervention in payout decisions and risk adjustments becomes impossible to manage once you exceed 100-200 active traders, creating dangerous bottlenecks that can delay withdrawals and damage your reputation.

Book a Prop Firm Infrastructure Audit to receive a breakdown of your current or planned structure, identification of risk, payout, and scaling bottlenecks, a recommended infrastructure setup based on your business model, and a system roadmap for launch or scaling readiness.

.png)