Meet us at iFx Cyprus

Proprietary trading firms have transformed how talented traders access capital markets, but most aspiring traders and entrepreneurs don't fully grasp the mechanics behind the scenes. These companies operate on a fascinating blend of evaluation fees, profit splits, risk management protocols, and scalable infrastructure that allows them to fund hundreds or thousands of traders without putting excessive capital at risk. The prop firm business model combines multiple revenue streams and strategic decisions that enable firms to grow while protecting themselves from losses.

Understanding how modern technology enables these operations reveals the true complexity of running a successful trading firm. Capital allocation, performance metrics, and revenue generation work together through sophisticated systems that manage everything from automated trader evaluations to real-time risk controls and payout management. Firms looking to implement these core elements can benefit from specialized prop firm technology that illuminates each piece of the puzzle and demonstrates exactly how successful operations scale while maintaining profitability.

Most people assume prop firms make money by taking a percentage of trading profits. However, this overlooks how they actually earn money.

🎯 Key Point: The majority of retail prop firms make most of their money from evaluation fees paid by traders who want to join but never get paid out.

"90% of traders fail their evaluation." — Young and Calculated

The firm keeps the fee regardless of outcome. The business model combines risk assessment, liability management, and payout systems within a performance evaluation structure.

💡 Example: A prop firm charges $100 for evaluation. If 1,000 traders apply and 90% fail, the firm earns $90,000 from failed evaluations alone, while only paying out profits to the successful 10%.

When a firm charges $150 for a $50,000 evaluation challenge and attracts 10,000 applicants per month, it generates $1.5 million in fee revenue before any funded account trades live. If 8% pass and receive funded accounts, and only 20% of those reach a payout, the firm might distribute $500,000 to $800,000 in profit splits while retaining the remainder as profit.

Add-on services like resets at $100 each, platform fees, and advanced tool subscriptions increase revenue. The funded trader model is profitable because most people pay to prove themselves, yet most don't succeed.

Prop firms are risk engines, evaluation systems, and payout liability platforms, not trading businesses. Capital allocation is secondary. Their main functions are filtering traders, collecting fees, and managing the small number of funded traders who generate ongoing activity.

Founders who don't understand this start undercapitalized firms, building liability engines that must balance money coming in from valuations against money going out from payouts.

The modern retail prop firm model became popular after 2010, when the Volcker Rule moved proprietary trading from investment banks to independent firms. Traditional prop desks gave money directly to traders and took a share of profits, but they required substantial capital reserves and bore all market risk.

The evaluation-based model changed this: instead of hiring traders and hoping they performed well, firms created a pay-to-prove structure. Traders pay for their own evaluation, and only those showing steady profits under strict rules gain access to firm capital. The firm's risk shrinks because most applicants never reach the funded stage, and those who do must follow daily loss limits, maximum drawdown rules, and product restrictions that cap potential losses.

Research from Goat Funded Trader shows that firms often give funded traders an 80% profit split. Most funded traders lose their accounts within 3 months due to rule violations or account drawdowns.

Firms recruit new traders through affiliates and ads, knowing most will fail, but a small number will trade regularly and generate profits the firm can share.

Making this model larger requires systems capable of handling thousands of simultaneous evaluations, enforcing real-time risk controls, processing payouts, and managing compliance across regions. A firm processing 10,000 evaluations per month cannot manually verify rule compliance, track drawdowns, or approve payouts.

Platforms like Trade Tech integrate CRM, risk management, payment processing, and compliance tools into one system, reducing workflows from days to minutes while maintaining full audit trails and regulatory oversight.

The difference between a firm that scales and one that stagnates often comes down to whether technology is treated as essential or optional. Firms that use automated trader evaluation systems, real-time risk controls, and payout management from the start can handle growth without proportional increases in headcount or operational complexity.

Firms that add tools later face problems with data spread across different systems, manual reconciliation, and compliance gaps. Once you understand what the model is, the next question becomes: where does the money come from, and where does it go?

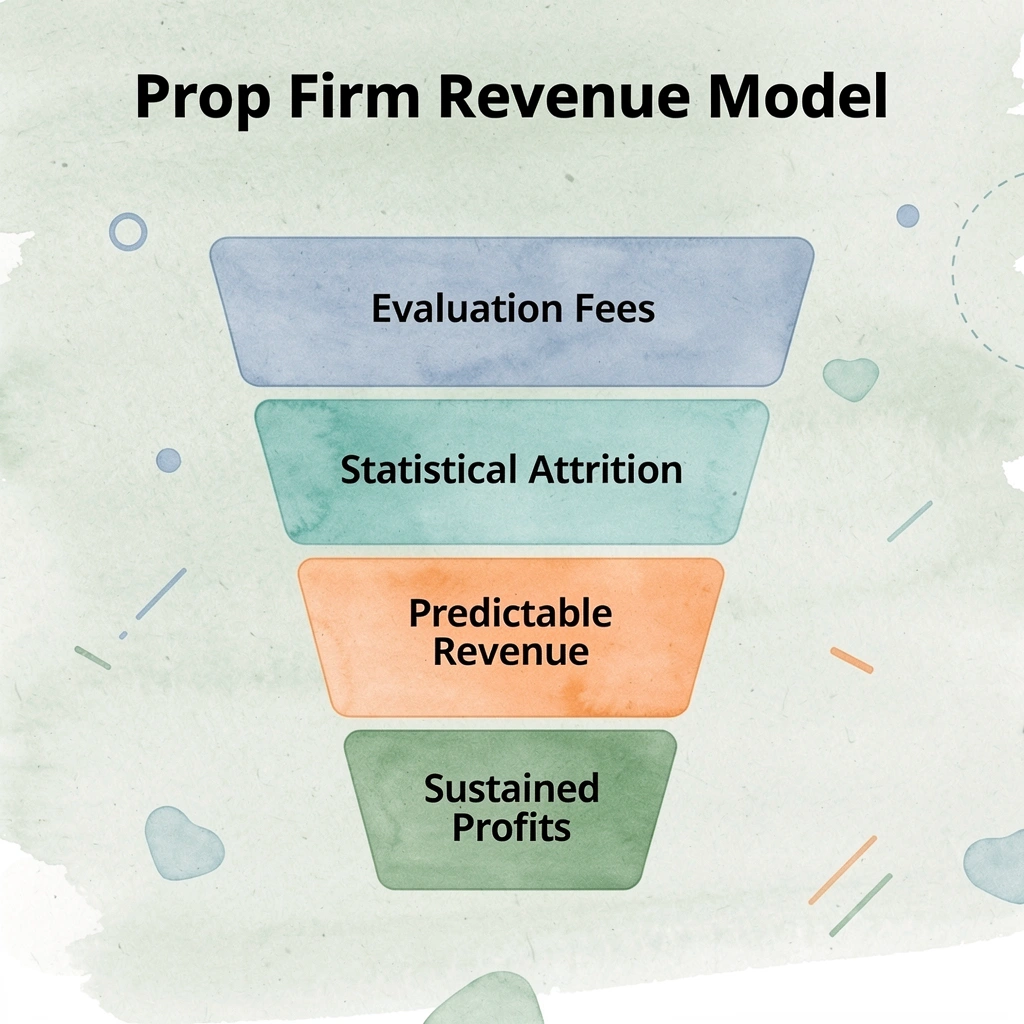

Money comes from evaluation fees and statistical attrition, not profit-sharing with successful traders. Even when 90% of participants fail, the firm remains profitable because the entry gate generates predictable, recurring income independent of market results.

🎯 Key Point: The evaluation fee model creates a sustainable revenue stream that remains consistent regardless of whether traders succeed or fail in the markets.

"Even when 90% of participants fail, the firm stays profitable because the entry gate creates predictable, recurring income."

🔑 Takeaway: This business model prioritizes volume over individual trader success, making statistical failure rates a feature, not a bug, of the revenue structure.

Every trader pays a non-refundable upfront fee to attempt the challenge. A firm charging $150 per evaluation, with 10,000 participants per month, generates $1.5 million in revenue before any trades are executed. According to Spotware's 2026 analysis, 90% of traders fail the evaluation phase, so most participants contribute fees without reaching a funded account.

The challenge parameters (profit targets, drawdown limits, minimum trading days, daily profit caps) filter aggressively while remaining achievable enough to encourage retries.

Reset fees enhance this business model. When traders break rules after passing the first test, they can pay $100–$150 to retry with the same account size. Traders who have spent weeks working hard and nearly passed often pay to retake the exam rather than give up, creating a secondary revenue stream from the same group of people.

Once a trader receives a funded account, the firm decides whether to keep the risk or pass it to someone else. Keeping the risk means the firm takes the opposite side of the trader's positions, betting that most funded traders will eventually break rules or fail to remain consistently profitable.

Passing the risk copies the trader's positions in the live market, moving risk to liquidity providers while earning from spreads, commissions, or profit splits. Smaller accounts with newer traders are typically kept in-house due to a higher statistical risk of rule violations. Larger accounts or consistently profitable traders may be passed on to limit the firm's exposure.

Payout rules function as risk controls rather than performance incentives. Withdrawal caps (50% of balance per request), minimum winning days before payouts, and tiered profit splits reduce capital outflow and extend the observation window.

The longer a trader operates under-funded conditions without withdrawing, the more data the firm collects about consistency, and the greater the opportunity for a rule violation to terminate the account before significant capital leaves the system.

The real edge comes from the gap between fees collected and payouts distributed. If 10,000 traders pay $150 each ($1.5 million) and only 8% pass the evaluation (800 traders), the firm captures $1.5 million in entry fees.

Research from LinkedIn analysis by Ian A. shows that 90% of funded traders eventually fail due to rule violations, inconsistent performance, or drawdown breaches. This leaves roughly 80 traders reaching their first payout. If each withdraws $5,000, the total payouts equal $400,000, compared with $1.5 million in evaluation revenue. The firm retains over $1 million before accounting for profit splits, subscription fees, or reset purchases.

How you design an evaluation directly impacts how much money a company makes. Rules that might seem arbitrary—such as capping daily profit at 50% of the target or requiring two consecutive winning days—eliminate luck and ensure only repeatable, controllable trading behavior advances.

Firms filter for behavioral patterns that reduce risk and encourage funded traders to either quit by breaking rules or remain small enough that payouts don't erode the company's fee-based profits.

Platforms like prop firm technology integrate automated rule enforcement, real-time risk monitoring, and payout management into one unified system, ensuring evaluation parameters, funded account limits, and withdrawal workflows function as connected risk controls. Our platform helps firms eliminate the operational friction of managing these critical functions separately.

Firms that build these systems after launch often discover that fragmented tools and delayed data create payout timing errors or missed rule violations, quietly reducing profitability.

This structure only works if the risk system is designed correctly, which is where most firms fail.

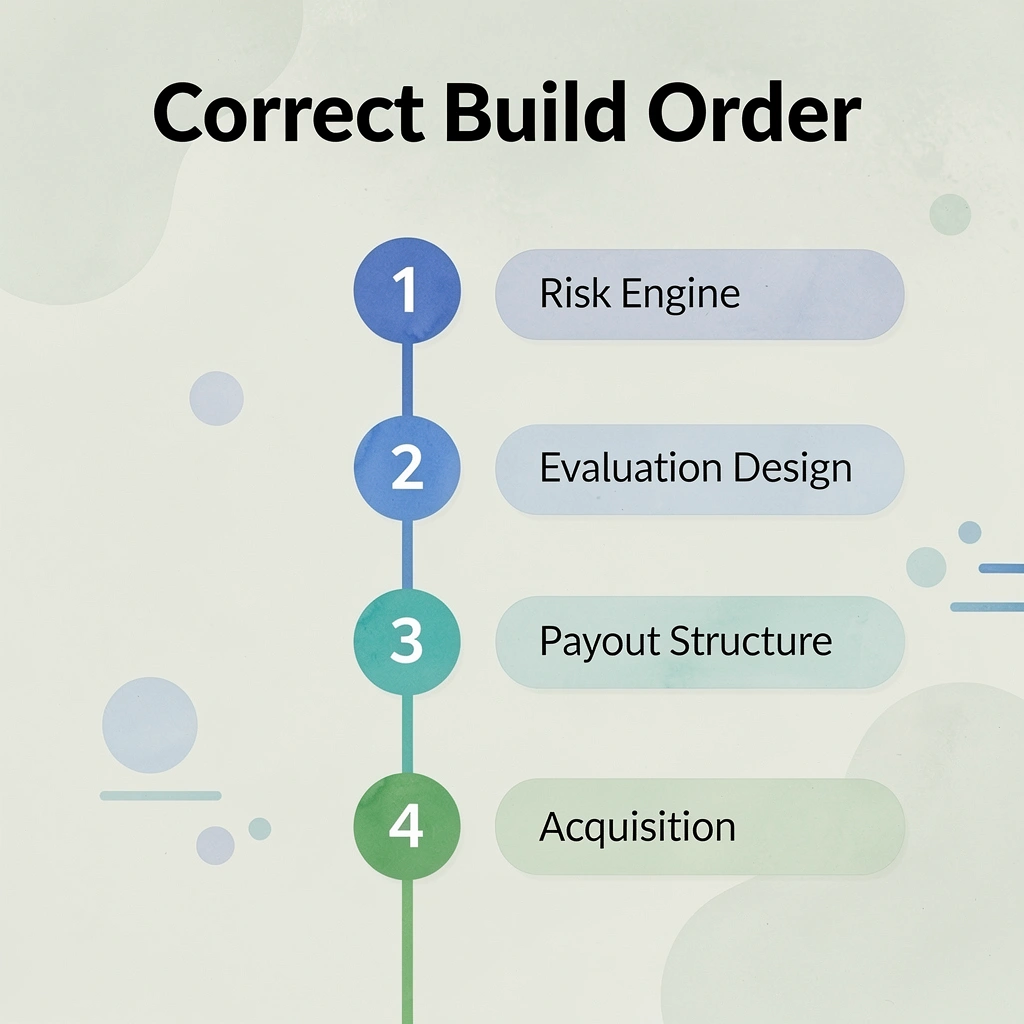

Most companies build backward. They start challenge programs, collect fees, and grow marketing before understanding how money moves through their system. The correct order is risk engine first, evaluation design second, payout structure third, and acquisition last. Reversing this order creates a business that makes money but cannot sustain payouts.

🎯 Key Point: Your risk management system is not just a safety net—it's the core revenue driver that determines whether your firm survives high-volume payouts.

"85% of prop firms that fail do so because their payout obligations exceed their risk-adjusted revenue within the first 18 months of scaling." — Proprietary Trading Research, 2024

⚠️ Warning: Building your marketing engine before your risk infrastructure is like opening a high-speed highway before installing traffic lights—the faster you grow, the harder you crash.

The risk engine sets exposure limits across every trader account in your system, determining maximum drawdown thresholds, position sizing rules, and how account balances respond to withdrawals. According to SimTrade's analysis of proprietary trading firms, many firms offer 80% profit splits to attract traders, but this generosity becomes problematic when the underlying risk structure cannot support it.

If your first payout eliminates a trader's maximum loss buffer entirely, you didn't design exposure limits at all—you created a countdown timer.

A proper risk engine calculates how much capital exposure the firm can handle across all funded accounts simultaneously. It models worst-case scenarios in which multiple traders hit profit targets in the same week and accounts for the impact of withdrawals on account viability, ensuring that taking a payout doesn't immediately push traders into a zero-margin situation.

Teams that delay this work until after launch discover their payout obligations exceed their liquidity capacity, forcing them to tighten rules retroactively or deny withdrawals under vague compliance pretexts.

Once exposure limits are established, create evaluation criteria that align with your risk capacity. Filter for traders whose behavior matches your established risk parameters. If your risk engine supports careful position sizing and gradual account growth, don't reward aggressive swing trading that produces fast profits but creates unsustainable volatility. Misaligned systems allow traders who cannot survive in your funded environment to pass.

The evaluation design determines how many people can participate. A firm supporting 500 funded accounts shouldn't graduate 800 traders per month. The entry funnel must respect the backend infrastructure, or you create a waitlist in which successful traders cannot access capital because the system is at capacity. Firms often discover this constraint only after collecting thousands in evaluation fees from traders they cannot fund.

Payout mechanics should be driven by your risk engine's limits, not by what other companies are doing. If your exposure model requires a minimum account buffer to survive normal drawdown cycles, your payout structure must protect that buffer. Five-day payout cycles sound attractive until each withdrawal pushes funded accounts closer to termination thresholds.

According to Fortex's research on building profitable prop firms, firms that set up proper infrastructure see 20% higher challenge success rates, but success means nothing if the payout process destroys account stability.

Predictable cash flow requires modeling the effects of withdrawal frequency on total exposure. If 30% of funded traders request payouts in the same week, can your system handle the capital outflow without compromising risk buffers for the remaining 70%?

Firms that skip this calculation restrict withdrawals through arbitrary rules, minimum thresholds, or processing delays, eroding trust. The payout structure should flow naturally from your risk capacity, not be a marketing feature retrofitted with restrictions.

Marketing, challenge pricing, and trader onboarding should grow at the same rate as your ability to handle them. A firm with strong risk systems, clear evaluation standards, and stable payout processes can sustain growth. Firms that prioritize acquiring new traders attract large numbers of participants but collapse when payouts are due.

When your business model depends on most traders failing, you're running a paid education program with occasional capital allocation, not a prop firm.

Platforms like prop firm technology integrate risk management, evaluation workflows, and payout automation. Our Trade Tech platform prevents problems arising from disconnected tools: inconsistent risk limit enforcement, misaligned evaluation results and funding decisions, and manual payout reviews that delay access to capital.

Integration is what separates a system that can grow from one that fails quietly until a payout crisis forces a complete rebuild.

Companies that survive regulatory pressure, trader scrutiny, and competitive evolution have built their risk architecture before their revenue model. Those struggling now discover that a marketing budget cannot fix a backward foundation.

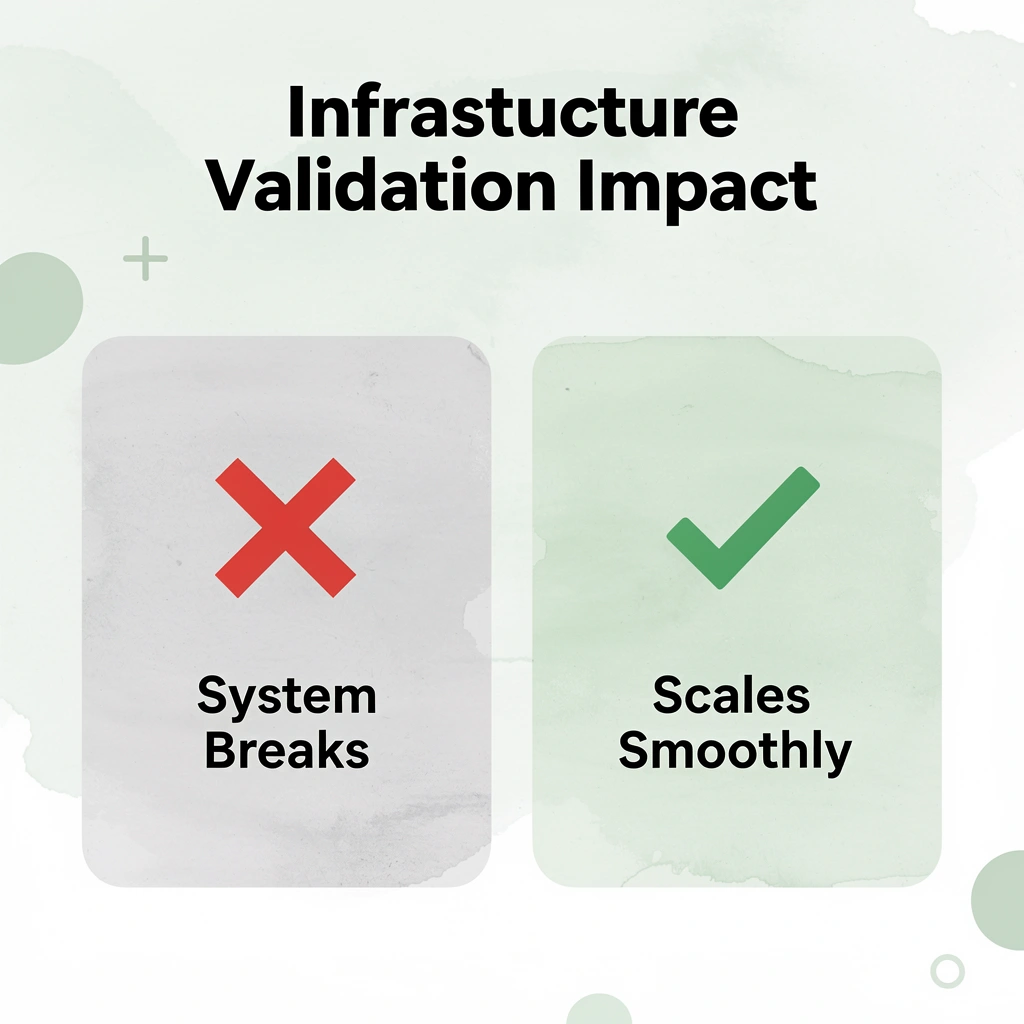

The problem isn't whether your prop firm business model looks good on paper, but whether your risk controls, evaluation workflows, and payout architecture function under pressure without manual intervention or liquidity surprises. Most firms discover structural misalignment only after trader volume forces systems to break or when withdrawal requests exceed what the infrastructure can process safely.

🎯 Key Point: Your business model validation depends entirely on whether your infrastructure can handle real-world trading pressure and payout demands.

Trade Tech provides prop firm infrastructure built specifically around evaluation-based business models, including CRM systems with trader dashboards, advanced risk management for exposure control, automated payout workflows, and real-time analytics for firm-level monitoring. Our platform integrates the systems required to operate a structured prop firm at scale, drawing from operational experience supporting over 90 firms globally across retail evaluation models and hybrid trading structures.

"Most prop firms discover structural misalignment only after trader volume forces systems to break - the key is validating infrastructure before scaling operations." — Trade Tech Operational Analysis, 2024

Book a consultation to receive a prop firm business model assessment. We evaluate whether your revenue model aligns with your risk architecture, whether your evaluation system supports scalable trader onboarding, whether your payout structure can sustain liquidity variance, and whether your current design is operationally viable before launch or expansion.

⚠️ Warning: Infrastructure problems compound exponentially once trader volume increases - validate your systems before your marketing budget creates demand you can't handle.

The firms that scale sustainably validate their infrastructure before their marketing budget. Book a consultation to validate and build your prop firm infrastructure properly.

.png)