Meet us at iFx Cyprus

The dream of launching a prop trading company comes with a harsh reality: most founders burn through capital in the first year by skipping the fundamentals. Understanding how to start a trading company means more than just having market knowledge or coding skills. It requires building the right legal framework, choosing scalable technology, establishing risk management protocols, and creating trader evaluation systems that actually work. Success depends on having the right structure, systems, and strategy from day one to avoid costly beginner mistakes and build a business positioned for long-term growth.

Specialized technology becomes the competitive advantage that separates thriving firms from failed ventures. Rather than piecing together mismatched software or spending months building custom solutions, successful founders rely on proven systems that handle trader management, challenge platforms, payment processing, risk controls, and compliance tools seamlessly. This integrated approach allows founders to focus on what matters most: attracting talented traders and growing funded accounts with reliable prop firm technology.

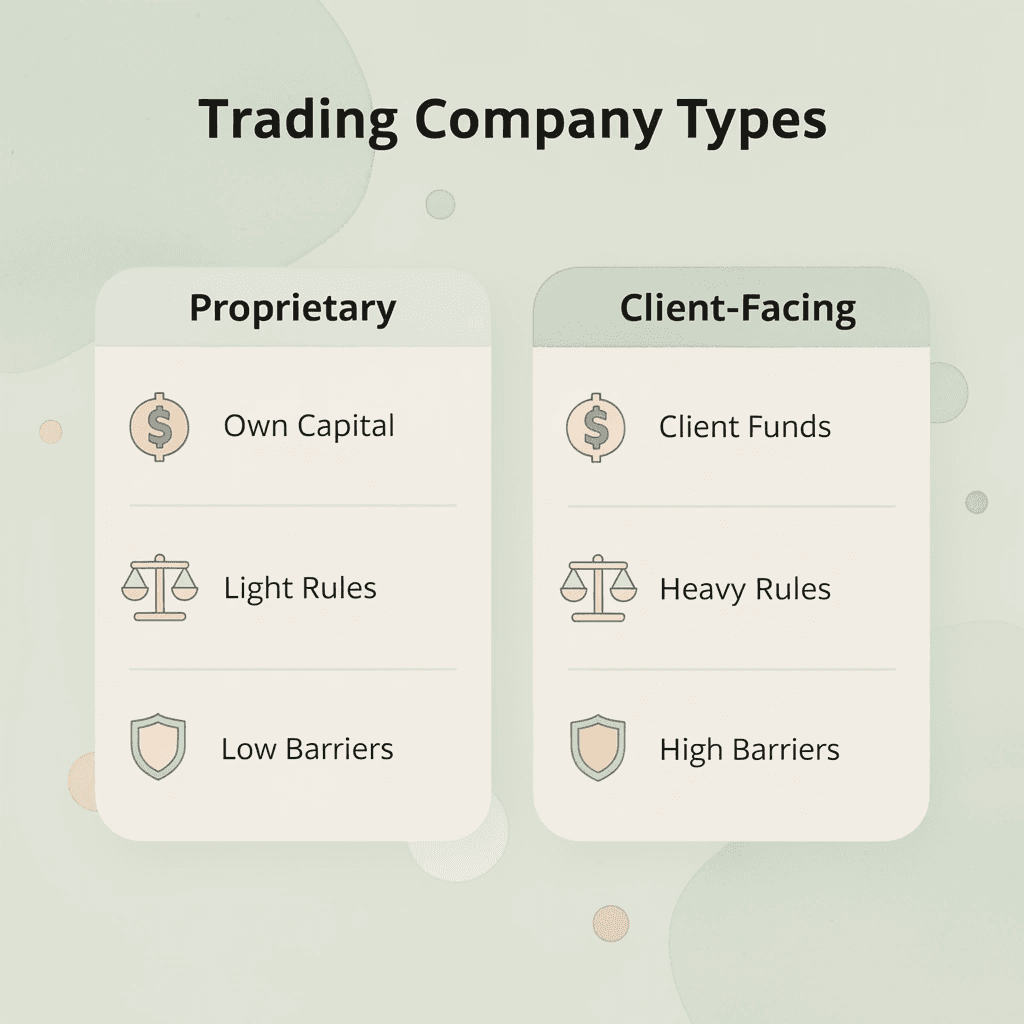

Yes, you can start a trading company without being a licensed broker or managing billions in client capital. You're building a proprietary trading operation that uses internal capital to profit from market activity, not a brokerage or investment advisory firm. Regulatory barriers that stop new founders from applying mainly to firms handling client money or giving investment advice. Structure your business correctly, and you avoid most of those requirements.

🎯 Key Point: Starting a proprietary trading company requires significantly fewer regulatory hurdles compared to client-facing financial services.

"Proprietary trading firms operate with their own capital and face minimal regulatory oversight compared to investment advisors or broker-dealers." — Financial Industry Analysis, 2024

⚠️ Warning: While regulatory requirements are lighter for prop trading, you still need proper business structure, risk management protocols, and compliance procedures to operate successfully.

The term carries weight because it encompasses a wide range of business models. A brokerage firm charges fees to help clients buy and sell investments. An investment management company builds investment plans for outside money. A prop trading firm does neither: it uses its own money, manages its own risk, and keeps its own profits.

According to The Kaplan Group, 50% of small businesses fail within five years, but prop firms collapse differently: from poorly managed risk exposure rather than insufficient customers. Your business problem isn't marketing or sales velocity. It's building systems that absorb trader losses without bleeding money faster than you generate profits.

Most people who want to start a trading company picture a desk with multiple monitors and capital to invest. What they overlook is the infrastructure required: legal contracts that protect the company when traders violate rules, relationships with brokers who execute large volumes of trades, and compensation systems that motivate traders while safeguarding the company.

82% of small businesses fail due to cash flow problems, and prop firms experience this through a specific mechanism: payout obligations arrive on schedule while trader profitability arrives in volatile, unpredictable clusters. Even profitable months can create liquidity crises if your capital reserve cannot absorb the timing mismatch.

You need a proper legal entity, even without client capital. Sole proprietorship exposes your personal assets to business liability. An LLC or corporation creates separation, enables enforceable trade agreements, and establishes the tax structure that determines whether you keep 70% or 45% of profits. Jurisdiction matters because regulatory interpretation varies. Some regions classify prop trading as an investment activity requiring licensing, while others recognise it as principal trading exempt from advisory rules. This distinction hinges on whether you're managing outside capital or deploying your own balance sheet.

Capital requirements fund survival during drawdown periods, not trades themselves. If you fund 20 traders at $50,000 each, you're not risking $1 million on markets—you're committing to payout cycles and operational overhead while most traders lose or break even and a small minority generates all profit. Variance creates cash flow stress even when overall performance is positive. A trader hits a $10,000 profit target on Monday, and you owe an immediate payout. Three other traders lose $8,000 combined over the next two weeks. The net is positive, but liquidity is negative if you cannot bridge the gap.

The biggest operational threat isn't hiring unprofitable traders. It's designing risk parameters that traders can exploit, or that fail to control correlated exposure. Weak max-drawdown rules let one trader's bad week erase a month of solid profit.

Scaling plans that fund too many traders in the same strategy create concentration risk when that strategy encounters adverse conditions. Overly lenient challenge calibration floods your firm with funded accounts before you've stress-tested payout capacity. When traders cluster around the same market conditions or correlate their entries, your exposure multiplies until a single market move triggers simultaneous drawdowns across your funded base.

Revenue looks deceptively healthy until you map payout timing against actual cash position. A firm can show $100,000 in monthly trading profits while facing $120,000 in payout obligations because prior months created liabilities that are now coming due. Firms collapse even when they appear profitable on paper because they optimise for revenue optics rather than liquidity management.

The business model works only when your risk infrastructure prevents concentration of risk, and your capital reserve absorbs the natural variance between traders' earnings and payout obligations. The real question is how much capital you need to survive those first critical months.

A trading company is a capital allocation machine with multiple layers of controls. Money comes in from managing risk across traders while maintaining sufficient cash to pay winners before losers deplete reserves. The system either generates greater profit by managing risk exposure or breaks down when a component fails.

🎯 Key Point: The entire operation hinges on precise risk management and capital flow timing - pay the winners before the losers drain your reserves.

"Successful trading companies operate as sophisticated capital allocation machines where risk management across multiple traders determines survival." — Trading Operations Analysis, 2024

💡 Critical Insight: This operating model requires constant monitoring because one failed component can collapse the entire system, regardless of how profitable other parts may be.

Trader acquisition funnels bring volume, but evaluation systems determine survival. Most firms test candidates under constrained conditions: profit targets paired with maximum drawdown limits, minimum trading days, and consistency requirements. The goal is to identify traders who generate returns within risk boundaries similar to live capital conditions.

When evaluation criteria are too loose, high-variance traders pass through, creating concentrated exposure. When criteria are too strict, you reject stable performers and starve the funded pipeline. According to 2023 prop firm data, only 7% of evaluation participants reach the payout stage, yet 100% pay challenge fees. The filtering efficiency is the core economic engine.

Once traders pass the evaluation, the funded stage begins. This is where firms either make sustainable profit or accumulate correlated risk they cannot detect until it becomes critical. Allocation decisions depend on a trader's history, strategy type, and the correlation between that trader's positions and those already funded.

The math breaks when multiple traders run similar strategies during the same market conditions. Individual risk limits mean nothing if ten funded accounts all short the same breakout pattern during a volatility spike. Centralized oversight across all positions determines whether a drawdown results in a recoverable drawdown or an operational failure.

Every layer described above—evaluation tracking, live trade monitoring, risk aggregation, payout calculation—depends on integrated infrastructure. Early-stage firms typically piece together separate tools: one platform for challenges, another for broker data, spreadsheets for risk checks, and manual processes for payouts. This approach works until it doesn't.

The breaking point comes around 50-100 funded traders. Manual oversight cannot track position correlation in real time; payout errors create disputes; and risk rule enforcement becomes inconsistent because it depends on someone noticing a breach rather than on automated controls.

Firms building everything in-house face months of development before scaling, while those using platforms like Trade Tech compress that timeline by centralizing evaluation, risk management, and payout systems into a single operational layer, eliminating vendor coordination overhead that typically consumes founders' attention during critical growth phases.

Profit splits between the firm and trader must balance competitive appeal with business sustainability. If the split is too generous, strong trader performance doesn't guarantee firm profitability. If the split is too restrictive, retaining traders becomes difficult, as proven traders will seek better terms elsewhere.

The distribution system controls when cash is paid out through weekly payout caps, maximum withdrawal limits, and gradual increases tied to consistent performance. These rules prevent cash flow problems from unusual months and function as risk controls, not merely payment mechanisms. But knowing how the system works and building one that survives contact with real market conditions are entirely different challenges.

Starting a prop trading firm requires a working capital allocation system before traders begin. Each decision limits what comes next: choose your funding model wrong, and your risk framework won't fit. Skip legal structure, and you can't make contracts with liquidity providers or handle payouts. Most failures stem from building things in the wrong order.

💡 Tip: Create a detailed implementation timeline mapping dependencies between foundational elements. Your legal structure must be finalized before establishing banking relationships or signing technology vendor agreements.

⚠️ Warning: Rushing the setup phase creates costly structural problems that become exponentially more expensive to fix once traders manage capital.

"The majority of prop trading firm failures occur within the first 18 months due to inadequate foundational planning and improper sequencing of critical business components." — Trading Industry Research, 2023

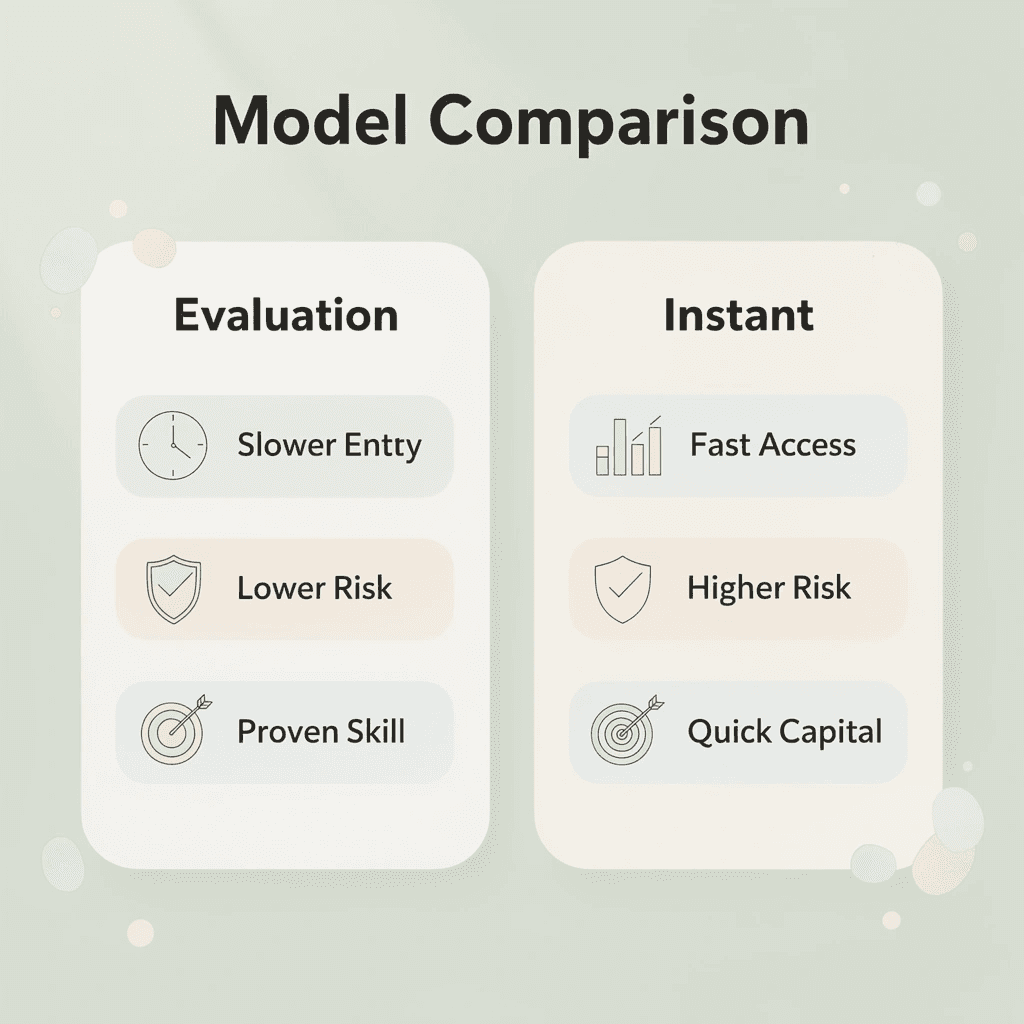

Your funding model decides everything that follows. Evaluation-based models require traders to pass multi-phase challenges before accessing capital, generating revenue from challenge fees, and extending the funding timeline. Instant funding models provide immediate capital but demand tighter risk controls, as unproven traders gain faster access to real accounts. Hybrid structures mix internal capital with funded trader programs, spreading risk while adding operational complexity. This choice locks in your risk exposure profile, scaling constraints, and revenue timing.

The model also affects how traders make money. Evaluation companies generate cash flow from challenge purchases regardless of pass rates. Instant-funding companies depend entirely on profit splits from successful accounts, so poor risk design creates an immediate capital drain. According to a 2023 analysis by the Proprietary Trading Firms Association, evaluation-based firms maintain 60% higher gross margins but face steeper trader acquisition costs due to lower pass rates.

You cannot work with liquidity providers, connect broker APIs, or handle payouts without a registered business entity. Most prop firms operate as limited liability companies or similar structures, depending on their location. Without legal registration, you cannot open business brokerage accounts, sign data feed agreements, or establish relationships with payment processors. One founder spent three months building a trader dashboard before discovering that no payment provider would work with an unregistered entity, forcing a complete timeline reset.

The way you set up your business affects taxes, personal liability, and growth potential. An LLC lets profits pass through to you and protects your personal assets, but it can complicate ownership sharing if you seek funding later. A C-corporation makes it easier to attract investors but subjects both the company and its owners to profit taxes. Your business structure determines how you split profits, handle government paperwork, and grow your operations. Talking to a business lawyer or accountant now means you won't have to rebuild your business structure later, when things get complicated and changes become expensive and difficult.

Your evaluation rules are your economic filter. Set profit targets too high, and pass rates drop below sustainable levels, killing trader acquisition momentum. Set drawdown limits too loosely, and funded traders blow accounts faster than challenge fees can cover losses. The math must balance evaluation difficulty, pass rate, and the profitability of funded traders. A 7% pass rate works if challenge fees cover operational costs and the 7% who pass generate positive expectancy. A 15% pass rate demands tighter-funded account controls or higher profit split retention to maintain unit economics.

Consistency requirements separate lucky streaks from repeatable skill. Requiring a minimum number of trading days prevents traders from meeting targets through single high-risk bets. Daily loss limits contain volatility that could otherwise wipe out accounts in a single session. Traders who meet strict consistency requirements typically experience lower drawdowns in funded accounts, reducing the capital at risk. The evaluation system serves as your first line of risk management, functioning before firm capital enters the market.

Risk controls determine whether your best traders become your biggest problems. Per-trader exposure limits cap how much capital any single account can lose before automatic cutoff. However, individual limits miss correlation risk: when ten funded traders use similar momentum strategies, a single bad move hits all positions simultaneously, creating portfolio-level drawdown that individual limits don't catch.

Centralized position monitoring across all funded accounts reveals hidden concentrations before they become losses. Our Trade Tech platform provides real-time visibility into correlated positions across your entire trader base, helping you manage systemic risk that traditional per-account limits miss.

Most prop firms that survive long-term use scaling rules tied to how stable a trader's performance is, not merely how much profit they make. A trader who makes $10,000 in one month through high volatility receives smaller increases than one who makes $3,000 monthly for six months with minimal drawdown. The consistent performer demonstrates risk-adjusted skill; the volatile performer might be getting lucky.

Scaling rules must distinguish between stable and unstable traders because allocating capital to unstable traders increases downside risk without commensurate upside potential. Correlation monitoring and performance-based scaling serve as the primary controls, supported by news-event restrictions, maximum position-size limits, and lists of prohibited instruments.

Manually tracking challenge progress, monitoring risk limits, and processing payouts quickly break down. One firm founder spent 60 hours weekly on spreadsheet updates and manual compliance checks before recognizing the model was unsustainable.

Modern prop firms depend on systems that automate challenge phase transitions, flag rule violations in real time, and trigger payout workflows when traders meet eligibility thresholds. Without this infrastructure, operational overhead scales linearly with the number of traders, thereby capping growth and creating error-prone manual processes.

Most founders face a choice between building and buying. Building your own systems lets you customize them, but requires months of development time and ongoing maintenance. Platforms like prop firm technology integrate challenge tracking, risk monitoring, CRM, and payment processing into one system. Our Trade Tech platform compresses setup from months to weeks and eliminates the need for multiple vendors. The real question: do you want to run a software company that happens to fund traders, or a trading company that uses software as infrastructure? For most, the latter makes more sense. But even the best infrastructure won't save you if no one shows up to use it.

Prop firms don't fail because traders lose money; they fail because their systems can't handle many failures simultaneously. One trader hitting their maximum loss limit is manageable. Ten traders doing it at once while the payout line lengthens and correlation goes undetected? That's a systems failure masquerading as a trading problem.

"The majority of prop firm failures stem from inadequate risk management systems rather than individual trader performance." — Trading Risk Management Institute, 2023

🎯 Key Point: The real danger isn't individual losses—it's when multiple risk events happen simultaneously, and your monitoring systems fail to detect the correlation patterns that amplify losses.

⚠️ Warning: Many firms focus exclusively on trader education while neglecting the infrastructure upgrades needed to handle concurrent risk events and payout obligations during volatile market conditions.

Money arrives in 30-day cycles from challenge fees, but funded traders expect weekly payouts. A successful month creates 40 new funded accounts, immediately increasing payout obligations, while revenue from those traders' challenge fees was spent two weeks earlier. The gap widens until the firm cannot meet its obligations. According to The Digital Leader, 70% of digital transformation initiatives fail because firms build customer-facing features while overlooking backend systems that prevent cash-flow collapse. The root cause isn't profitability—it's a liquidity mismatch between when money arrives and when it must go out. Solutions include delaying payouts to bi-weekly cycles, requiring minimum payout thresholds, or maintaining a cash reserve equal to 60 days of average payout obligations.

One firm lost everything when its payment processor froze accounts during a compliance audit with no backup system. Funded traders couldn't withdraw, new customers couldn't pay, and operations stopped for 11 days. The firm's reputation never recovered. This failure stems from single-vendor dependency for mission-critical infrastructure. When your CRM, payment gateway, risk monitoring, and broker integration each come from different vendors, you're managing four potential failure points. One breakdown halts the entire system. Platforms like prop firm technology centralize these functions in integrated systems, reducing vendor concentration risk while compressing coordination overhead from weeks to days. Our Trade Tech platform continues to operate even when individual components are disrupted, providing the architectural resilience your firm needs.

Regulatory changes don't announce themselves with flashing warnings. A jurisdiction updates KYC requirements. Your onboarding flow doesn't. Six months later, you're processing traders who shouldn't have been approved. The failure happens slowly, then all at once when regulators audit your records. The root cause is treating compliance as a one-time setup rather than continuous monitoring. The solution requires automated compliance tracking that updates as regulations change, flags accounts that no longer meet requirements, and maintains audit trails that prove you knew who you were funding and when. Manual spreadsheet tracking fails at scale because humans cannot monitor 200 jurisdictions simultaneously.

Adding 100 funded traders in a month may appear to be growth, but it introduces risk without evidence that traders can perform consistently over time. Early profits don't guarantee sustained returns—some traders get lucky; others pass evaluations by taking outsized risks that succeed once and then lose funded accounts within weeks. The core problem is distributing funded capital faster than you can validate a trader edge. Staged validation addresses this: traders must demonstrate consistent performance over 60–90 days before accessing larger amounts, and total exposure limits ensure funded capital doesn't exceed what your risk systems can monitor in real time.

Eight funded traders simultaneously short the same currency pair using similar entry signals, unaware of each other. Your firm's total exposure is 8 times what you thought it was. When the trade reverses, all eight hit drawdown limits within the same hour. The failure isn't that traders lost—it's that your system didn't detect the correlation before it became catastrophic.

You need automated monitoring that flags overlapping positions, similar entry timing, and correlated strategy patterns. Without this layer, you're running a casino where you don't know how much is on the table. But knowing what breaks only matters if you can build the system that survives contact with reality.

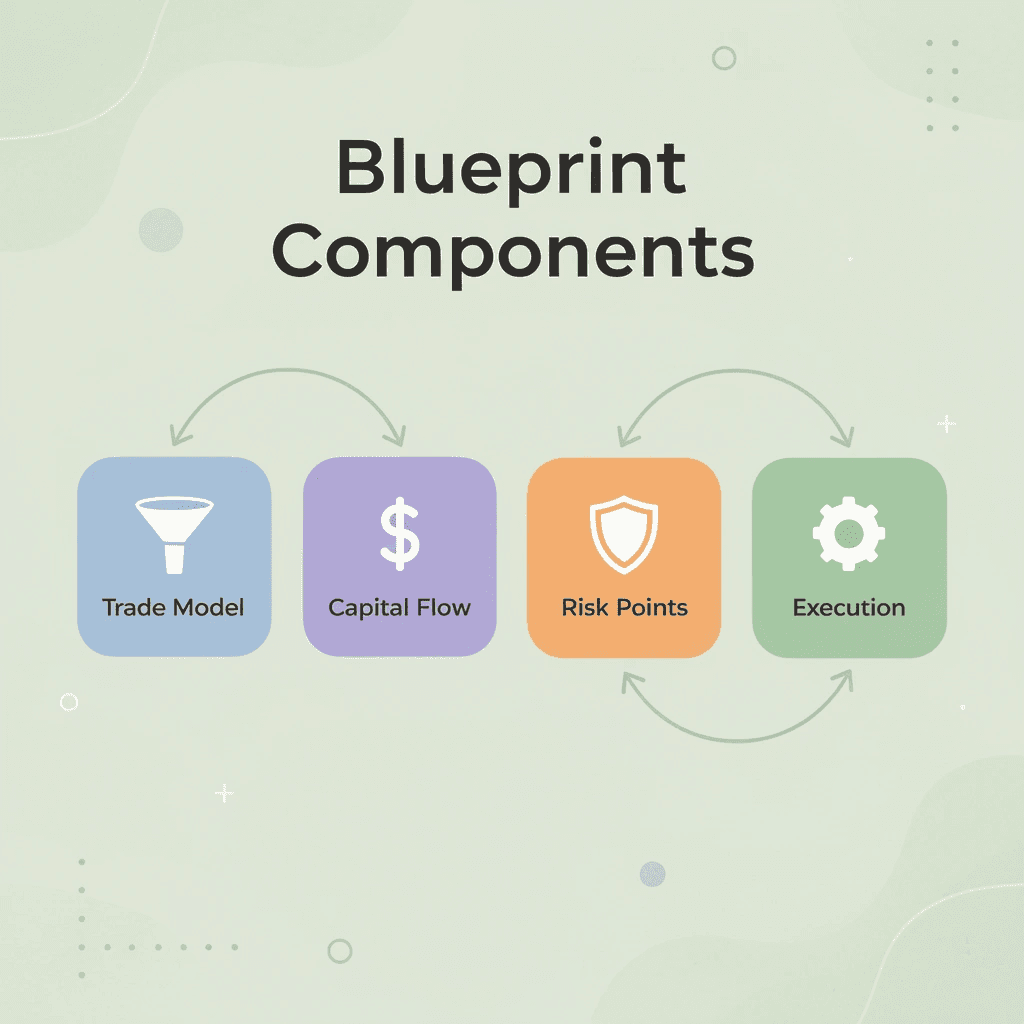

You need a structured blueprint that defines your trading model, maps your capital flow, identifies operational risk points, and outlines execution before committing resources. Without that critical clarity, you're building on assumptions that collapse under real market conditions.

🎯 Key Point: A five-minute blueprint exercise forces you to answer what truly matters: Are you running an evaluation funnel or an instant funding model? How does capital move from liquidity providers through your risk systems to trader accounts? Where do compliance checks, payout approvals, and position monitoring happen? These architecture decisions determine whether your infrastructure handles 50 funded traders or 5,000.

"Firms that successfully scale past the first year have one thing in common: they define their operational blueprint before growth stress-tests their assumptions." — Trade Tech Solutions Research, 2024

Firms that scale past the first year define their trade model (evaluation-based, instant funding, or hybrid), map capital structure (reserves versus active trader accounts), outline supplier relationships (broker integrations, payment processors, KYC providers), and identify operational risk points (cash flow timing, compliance bottlenecks, technology dependencies). This essential clarity serves as your reference point when growth stresses your assumptions.

💡 Tip: Platforms like prop firm technology let you build that blueprint in minutes rather than months. Our Trade Tech platform lets you define how CRM, risk monitoring, payment processing, and compliance tracking connect—where capital flows and what breaks first when volume doubles. That's the difference between a business plan and an operating system.

.png)